Kathleen Kinder brings over 11 years of experience in the research industry, with deep expertise in finance, cryptocurrency, and insurance. ... See full bio

Barry Elad is a finance and tech journalist who loves breaking down complex ideas into simple, practical insights. Whether he's exploring fi... See full bio

SBI Crypto will discontinue its Bitcoin mining pool service on July 31, 2026, according to Hiroaki Morita, CEO of SBI Crypto. The pool stops accepting mining shares at 07:00 JST that day.

Key Takeaways

SBI Crypto, the mining arm of Japan’s SBI Group, will end its mining pool service effective July 31, 2026.

The pool stops accepting mining shares at 07:00 JST, equal to 22:00 UTC the evening before.

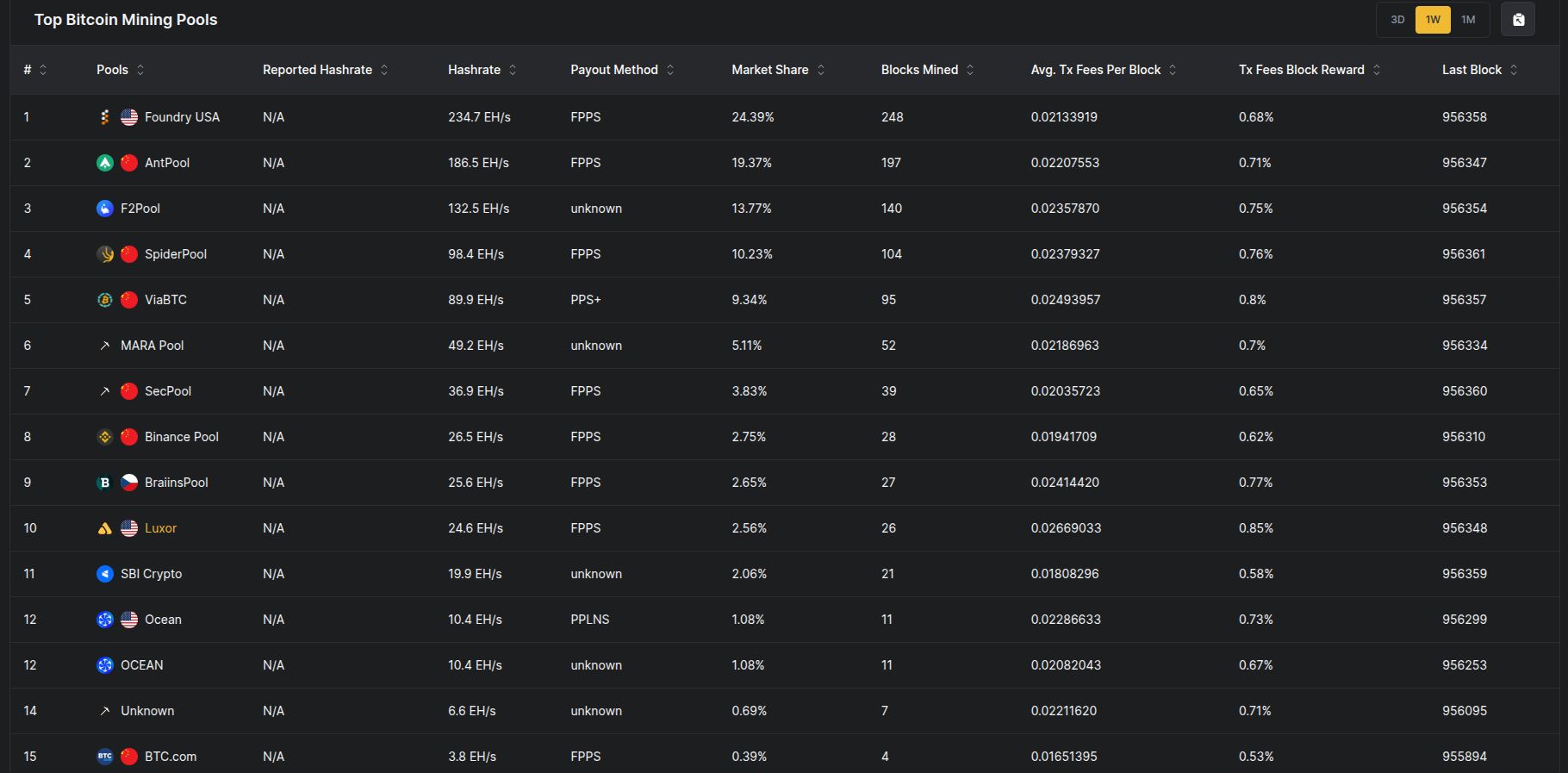

SBI Crypto, per Hashrate Index, currently controls 19.1 EH/s, or roughly 1.97% of Bitcoin’s network hashrate, ranking 11th among mining pools.

The notice names three alternative pool operators as reference options for displaced miners, but disclaims any endorsement or liability (Braiins, Luxor Pool, and NeoPool).

SBI Crypto’s exit, per Hashrate Index, adds to an already top-heavy market as Foundry USA, AntPool, and F2Pool together hold about 57.6% of network hashrate.

What Happened?

SBI Crypto has decided to discontinue its mining pool service, with operations ceasing on the Friday cutoff date. The announcement was signed by Hiroaki Morita, CEO of SBI Crypto Co., Ltd. It gives customers roughly four weeks’ notice.

The mining pool is scheduled to stop accepting mining shares at 07:00 JST on the cutoff date, which is 22:00 UTC the day before. That deadline effectively ends payouts tied to the pool’s infrastructure. SBI Crypto, per Hashrate Index’s live dashboard, is still running a meaningful share of global hashrate heading into the shutdown window.

THE BLOCK: SBI Crypto plans to discontinue its mining pool service at the end of July.

According to a company notice, the pool will stop accepting mining shares at 22:00 UTC on July 30, with final payout and operational details to be provided separately. pic.twitter.com/8A76dhfSll

Every connected miner must redirect hashing power elsewhere or go idle once the window closes. Notably, the notice does not disclose a reason for the shutdown.

For a subsidiary of SBI Group, a diversified Tokyo-listed financial conglomerate, an unexplained exit from a business line reads differently than it would from a standalone mining startup. The silence itself is the data point here.

Nothing in the primary notice points to a hack, a regulatory order, or a technical failure. Speculating on a cause the company did not state would misrepresent what the record actually shows.

Where the Hashrate Goes?

The announcement lists three alternative mining pool operators as reference options for customers: Braiins, Luxor Pool, and NeoPool. SBI Crypto does not endorse or recommend any particular provider and says it will not be liable for losses arising from the use of a third-party pool.

That reference list matters beyond a courtesy gesture. SBI Crypto currently runs 19.1 EH/s of hashrate, a 1.97% network share that makes it the 11th-largest Bitcoin mining pool. Naming its own displaced customers’ next home turns a routine wind-down into a direct handoff of real hashing capacity to specific named rivals, rather than letting that capacity scatter randomly across the market.

By the numbers, SBI Crypto’s exit removes an operator controlling 19.1 EH/s, about 1.97% of Bitcoin’s network hashrate, from the pool market at the cutoff. The notice steers that capacity toward three named alternatives, Braiins, Luxor Pool, and NeoPool, none of which SBI Crypto formally endorses.

The three largest Bitcoin mining pools, Foundry USA (24.43%), AntPool (19.41%), and F2Pool (13.79%), together control roughly 57.6% of network hashrate. SBI Crypto’s departure does not directly hand share to any single one of those three top pools; its notice points miners toward Braiins, Luxor Pool, and NeoPool instead.

But every exit from a mid-tier pool narrows the field of viable independent operators. In a market where the top three already exceed half of global hashrate, each additional consolidation event tightens a distribution that miners rely on to avoid pool-level censorship or 51%-adjacent risk, regardless of which specific pool absorbs the departed capacity.

Crypto exchange market share data shows a similar dynamic on the trading side of the industry, where volume concentrates among a shrinking set of dominant platforms even as new entrants launch. Mining pool economics follow a related logic: scale lowers payout variance, which pulls hashrate toward already-large pools over time.

Don't chase the news. Let us curate it.

You get one weekly briefing with only the stories that matter. If the market is quiet, we skip it.

✅ Join readers from Visa, Mastercard, Vanguard, and the FDIC.

CoinLaw’s Takeaway

This shutdown reads as an orderly wind-down rather than a distress signal, based on what SBI Crypto has actually disclosed. The company gave a specific cutoff date, named its own CEO on the notice, and pointed departing customers toward three functioning competitors instead of leaving them without direction. That is not how a pool typically exits after a hack or a regulatory shutdown, where operators tend to go quiet or freeze withdrawals rather than publish a clean, dated timeline.

The more interesting signal is what the notice omits. SBI Group operates across banking, securities, and asset management in addition to crypto mining, and a business unit inside that structure closing without a stated reason suggests a portfolio decision rather than an operational failure, though the notice itself does not confirm either reading.

What is verifiable is the redistribution. Roughly 19.1 EH/s of hashrate, currently 1.97% of the network, now needs a new home in a market where the top three pools already control roughly 57.6% combined. That 19.1 EH/s figure is the part worth tracking as the cutoff approaches, independent of why SBI Crypto made the call.

This article has been reviewed and fact-checked by

Barry Elad.

CoinLaw follows strict Publishing Principles and a documented Fact-Check Policy to ensure accuracy, transparency, and editorial independence across all content.

Add CoinLaw as a Preferred Source on Google for instant updates!

Kathleen Kinder brings over 11 years of experience in the research industry, with deep expertise in finance, cryptocurrency, and insurance. At CoinLaw, she writes timely, reader-focused news articles and also serves as a senior editorial reviewer. Drawing on her background in B2B research, consumer insights, and executive interviews, she ensures every piece delivers clarity, accuracy, and real-world relevance.

Disclaimer: The content published on CoinLaw is intended solely for informational and educational purposes. It does not constitute financial, legal, or investment advice, nor does it reflect the views or recommendations of CoinLaw regarding the buying, selling, or holding of any assets. All investments carry risk, and you should conduct your own research or consult with a qualified advisor before making any financial decisions. You use the information on this website entirely at your own risk.

To provide the best experiences, we and our partners use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us and our partners to process personal data such as browsing behavior or unique IDs on this site and show (non-) personalized ads. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Click below to consent to the above or make granular choices. Your choices will be applied to this site only. You can change your settings at any time, including withdrawing your consent, by using the toggles on the Cookie Policy, or by clicking on the manage consent button at the bottom of the screen.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.