In recent years, the microfinance industry has been pivotal in providing financial services to underserved communities, transforming the lives of millions worldwide. With small loans, savings accounts, and other financial products, microfinance institutions (MFIs) aim to bring financial stability and growth opportunities to individuals who lack access to traditional banking.

Today, the microfinance sector is poised for continued growth and innovation. This article explores key milestones, market forecasts, and critical data that illustrate the evolving role of microfinance in promoting financial inclusion and economic development worldwide.

Editor’s Choice

- The global digital wallet market is forecast to grow to $68.02 billion in 2026, up from $56.77 billion in 2025.

- Digital wallet users worldwide are expected to increase to 5.2 billion in 2026.

- RBI cut the risk weight on qualifying microfinance consumer loans to 100% from 125%, reversing the earlier 25-point increase.

- AI-based credit scoring improved women borrowers’ loan approval rates by 29.4% and reduced income-exclusion errors by 24.1%.

- The peer-to-peer lending market is expected to reach $327.18 billion in 2026, growing from $250.11 billion in 2025.

Recent Developments

- India approved a ₹200 billion credit guarantee scheme for microfinance firms in March 2026 to support sector stability.

- In India, the microfinance portfolio declined 3.53% year over year to ₹3,85,348 crore.

- Industry commentary in early 2026 cited stressed assets near ₹55,000 crore and headline NPAs around 16%.

- AI-driven lending models can improve default prediction by 18.6% in microfinance settings.

- India’s microfinance sector is expected to grow by 12%–15% in FY26.

Microfinance Market Growth and Forecast Insights

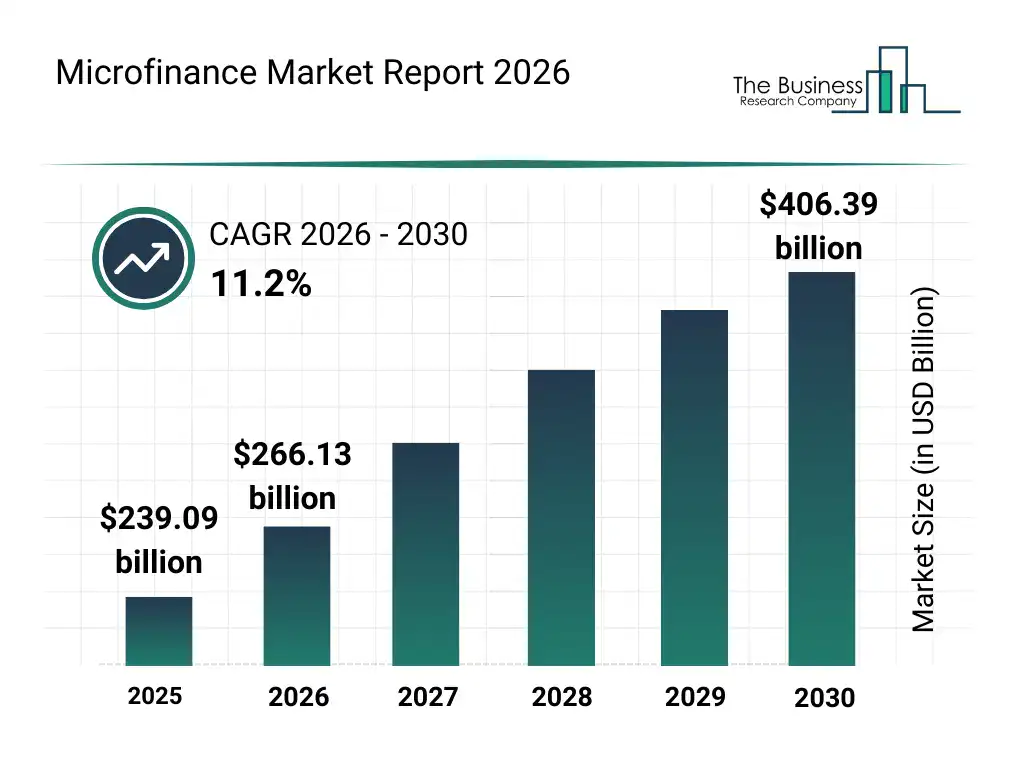

- The global microfinance market reached $239.09 billion in 2025, reflecting strong demand for financial inclusion services worldwide.

- The market will grow to $266.13 billion in 2026, marking steady year-over-year expansion.

- The industry will grow at a CAGR of 11.2% from 2026 to 2030, highlighting sustained expansion across emerging markets.

- By 2027, the market will surpass $295 billion, driven by increased adoption of digital lending platforms.

- In 2028, the microfinance market will reach approximately $328 billion, supported by rising SME financing needs.

- The market will expand to around $363 billion in 2029, as mobile-based financial services continue to scale.

- By 2030, the global microfinance market will hit $406.39 billion, underscoring long-term growth potential and investment opportunities.

- Overall, the market will add over $167 billion in value between 2025 and 2030, signaling rapid expansion and increasing global penetration.

Regional Insights and Analysis

- South Asia remains the largest microfinance region, with India accounting for nearly 35% of global microfinance clients.

- Sub-Saharan Africa’s microfinance institutions served 18 million clients, marking a 12% increase.

- Latin America and the Caribbean hold a 16% share of the global microfinance market.

- In the U.S. microfinance market, over 54% of microloans are distributed through digital platforms.

- In North America, digital lending accounts for over 60% of total microloan processing.

- Southeast Asia’s mobile fintech app penetration reached 49%, led by the Philippines at 63% and Indonesia at 49%.

- Mobile-based microlending in Southeast Asia has grown by about 32% annually since 2020.

Key Companies & Market Share Insights

- Grameen Bank reported 9.77 million members and 8.95 million borrowers in March 2026.

- Bank Rakyat Indonesia serves more than 35 million micro and ultra-micro borrowers and over 144 million micro deposit customers.

- BancoSol now serves 2 million clients in Bolivia.

- Compartamos Banco in Peru serves more than 1.4 million clients, with 85% of its portfolio dedicated to MSEs.

- Grameen Bank’s total loan disbursement reached $45.69 billion, with $3.39 billion in loans outstanding.

- 75% of IFC loan proceeds to Compartamos Banco will support women-owned MSEs, while women represent 76% of clients.

- Equitas Small Finance Bank’s gross advances reached ₹461.83 billion as of March 31, 2026, while deposits rose 7.96% year over year.

- KWFT serves over 800,000 clients across 229 offices in 45 of Kenya’s 47 counties.

Microfinance’s Role in Bridging Financial Inclusion

- About 1.3 billion adults remain unbanked globally, while 79% of adults now have a financial account.

- In low- and middle-income countries, 75% of adults have an account, up from 74% in 2021.

- Women make up 80% of microfinance clients worldwide, while 65% of borrowers live in rural areas.

- In South Asia, women represent 90% of microfinance borrowers.

- Digital loans accounted for 25% of total microfinance disbursements.

- Microloans have directly supported over 100 million women globally.

- Financial literacy training has reached more than 10 million borrowers worldwide.

- Around 300 million financial accounts remain inactive despite broader inclusion gains.

Client Demographics and Outreach

- Around 50% of microfinance borrowers live in rural areas.

- Low-income individuals account for 80% of microfinance borrowers.

- Youth-focused microfinance programs grew by 15%.

- In urban markets, 35% of borrowers use microloans for retail or trade businesses.

- Agricultural loans represent 30% of all microfinance products.

Financial Products and Services Offered

- Remittance services are offered by 40% of MFIs, and the digital remittance market is projected at $33.41 billion in 2026.

- Africa’s solar financing is expanding fast, with installations rising 54% year-on-year in 2025 and new solar PV capacity reaching about 4.5 GW.

- Microinsurance demand is rising, with the market valued at $95.15 billion in 2026 and more than 500 million microinsurance policies sold in the past decade.

- South Asia remains the largest microfinance market, with nearly 35% of global microfinance clients in India alone.

- Women account for about 80% of microfinance clients, reflecting the sector’s strong focus on female entrepreneurship.

- Pension products are gaining traction globally, with pension assets totaling $58.5 trillion at the end of 2024 across 22 major markets.

Microfinance Market Dynamics and Trends

- Blockchain enhances transparency in MFIs, with enterprise adoption driven by MiCA regulations and maturing tech.

- Digital wallets for microfinance transactions are forecasted to grow 30% annually due to smartphone penetration.

- ESG practices are integrated by 50% of institutions, boosting sustainable finance and investor demand.

- P2P lending market to reach $222.90 billion in 2026, expanding at 24.68% CAGR to 2035.

- 60% of MFIs offer youth-targeted microloans for young entrepreneurs.

- Impact investing rises, with MFIs attracting capital for poverty reduction via ESG and blended finance.

- 65% of clients are under age 35, fueling demand for digital and youth-focused products.

Sources of Funds by Legal Status of Microfinance Institutions

- Credit Unions rely most heavily on deposits, with 80% of funding from this source.

- Rural Banks depend largely on deposits, making up 70% of total funds.

- Banks fund through a mix, with 60% from deposits and 25% from borrowings.

- NGOs depend most on equity, accounting for 50% of funding.

- NBFIs have a balanced mix, with 40% from borrowings and 50% from deposits.

- Average MFIs source 55% from deposits, 30% equity, 25% borrowings.

Key Microfinance Institution (MFI) Performance Metrics

- Portfolio at Risk >30 days averages 4.2% across MFIs.

- Operating expense ratio for MFIs averages 20%, challenging for small loans.

- Portfolio Yield stands at 19.2%, the highest key metric for lending income.

- Return on Equity (ROE) is reported at 11.5%, a strong profitability indicator.

- Loan repayment rates average 97% globally for MFIs.

- Average MFI interest rates are at 39% effective on the total portfolio.

Challenges and Risks in the Microfinance Sector

- 10% of borrowers face over-indebtedness, taking multiple loans to cover debts.

- PAR >30 days averages 4.2% across MFIs amid economic volatility.

- Interest rate caps squeeze margins, reducing outreach and raising informal sector risks.

- Regulatory pressures intensify with stricter compliance worldwide.

- Indian MFIs saw 14% YoY portfolio decline and 95% profit drop in FY2025 stress.

- Phishing attacks surged with 2.4 million emails in H1 2025 targeting the finance sector.

- Delinquency 90+ days doubled, and overdue books surged in recent years.

- 97% repayment rates challenged by unsecured lending in volatile contexts.

Frequently Asked Questions (FAQs)

40% of microfinance institutions offer remittance services.

Global MFIs maintain an average loan repayment rate of 96%.

Asian MFIs dominate with over 60% of global microfinance assets.

Portfolio yield stands at 19.2%.

80% of credit unions’ funding comes from deposits.

Conclusion

As microfinance continues to grow, it plays a crucial role in empowering individuals, supporting small businesses, and driving economic development in regions lacking traditional financial services. With a strong trend toward digital transformation, the sector is expanding its reach and accessibility, especially among rural and unbanked populations. However, MFIs face challenges like operational costs, regulatory pressures, and the risk of client over-indebtedness.

Moving forward, innovations such as blockchain, AI-based credit scoring, and mobile-based financial services promise to reshape the microfinance landscape. As these institutions adapt to evolving demands and technologies, the microfinance industry is set to make a lasting impact on global financial inclusion efforts.

RSRita Simmons

Barry Elad, I must commend your comprehensive analysis on the ever-evolving microfinance sector. Your segment on ‘Microfinance’s Role in Bridging Financial Inclusion’ particularly stands out. It’s refreshing to see a deep dive into how these initiatives are genuinely making a difference in impoverished communities. Germinating financial inclusion through microfinance has indeed proliferated opportunities that were once deemed unattainable for many. Keep up the exceptional work!

Thank you for the kind words, Rita. The role of microfinance in financial inclusion is a topic we plan to keep revisiting as the data evolves and new program models emerge.

AJAlex Johnson

Not sure I agree with all this optimism. Sure, microfinance helps, but aren’t we overlooking the potential for debt traps? How effective are these programs in the long run?

That is a fair concern, Alex. Debt traps are a documented risk, particularly when borrowers take multiple loans from competing lenders. Long-term studies show mixed results depending heavily on program design, interest rate caps, and whether financial literacy support accompanies the credit. Institutions with the strongest outcomes tend to treat microfinance as part of a broader financial inclusion toolkit rather than a standalone product.

RSRita Simmons

Alex, that’s a valid point. The risk of over-indebtedness is indeed a concern. However, the key is in responsible lending and education.

Well put, Rita. Responsible lending practices and financial literacy support are the pillars that make microfinance sustainable rather than exploitative. Institutions that combine credit with education consistently show better repayment outcomes and lower rates of over-indebtedness.

TBTim B.

hey, so in the ‘Key Companies & Market Share Insights’ part, could you explain how these companies are actually chosen? Like what makes them stand out?

Good question, Tim. Companies are selected based on a combination of AUM, geographic reach, loan portfolio size, and availability of published impact data. Priority goes to institutions with verifiable third-party reporting and a track record of at least five years of operations.

DJDerek J.

I found the ‘Challenges and Risks in the Microfinance Sector’ segment to be quite lacking. There’s a lot more complexity to the risks involved that Barry Elad completely glosses over. It’s not just about operational risks, but also about the potential for systemic issues that could arise from market saturation and lack of regulation.

Fair point, Derek. Systemic risks from market saturation and regulatory gaps deserve more depth than a single section can accommodate. The 2010 Andhra Pradesh microfinance crisis in India is probably the clearest historical example of what unchecked growth without regulatory guardrails can produce. We appreciate the feedback and will look to expand that treatment.

SKSarah K

Absolutely thrilled to read about ‘Gender and Microfinance: New Insights’. It’s imperative that we continue to highlight and support initiatives that aim to empower women financially across the globe. Microfinance has often been a lifeline for many women in developing countries, offering them a path out of poverty and towards autonomy. Barry’s piece beautifully captures the essence and impacts of these programs. It’s uplifting to see how tailored financial products can truly make a difference. Hats off to microfinance institutions that are prioritizing gender inclusivity and helping women build more sustainable futures.

Thank you, Sarah. The data consistently shows that lending to women generates stronger community-level multiplier effects, which is why so many institutions have made gender inclusion a strategic priority rather than just a side initiative.